Table of Contents

2.3k

7 min

14.10.2025

From Seasonal Slumps to Steady Profit: How to Earn All Year Round

Kateryna Gulchenko

Senior Customer Support Manager

After every successful period comes a downturn — and you start looking for the reason again: clients seem less active, ads don’t work, the market has changed.

Sounds familiar? It happens even to experienced entrepreneurs.

But maybe the issue isn’t that your business is “unstable.” Maybe it’s simply seasonal — and you just haven’t factored that into your financial planning yet.

Let’s figure out what seasonality really is, why it affects your finances, and how to make demand fluctuations work for your business, not against it.

What Is Seasonality and Why It Affects Business Finances

Seasonality is the regular fluctuation of sales, demand, or expenses that repeats throughout the year.

Almost every business feels it:

- in retail — spikes before the holidays;

- in construction — activity in spring and summer;

- in services — vacation or holiday periods;

- in manufacturing — client order cycles;

- in e-commerce — peaks during sales and holiday campaigns.

It’s a natural phenomenon, but it significantly affects cash flow, inventory, team workload, and profitability.

That’s why the main goal of a business owner is not to avoid seasonality, but to learn how to account for it.

Why Seasonality Can Be a Risk

Many entrepreneurs ignore seasonal patterns, considering them “minor fluctuations.”

In some key industries — including retail, tourism, and agriculture — up to 70% of annual revenue comes from just a few months of peak season. — SCORE, official partner of the U.S. Small Business Administration (SBA)

This means that just a few months can determine the financial outcome of the entire year.

If seasonality is not factored into planning, a business risks losing stability even after its most successful period.

As a result, companies face typical financial problems:

- Cash gaps. During sales downturns, income isn’t enough to cover fixed expenses — rent, salaries, taxes. Even a profitable business can temporarily run out of funding.

- Excess purchases or product shortages. Without demand forecasting, you can either overstock (and freeze money in inventory) or run out of goods during peak sales.

- Team overload or downtime. During high season, the team can’t keep up; during low season, it’s underutilized — but salaries still need to be paid.

- Poor management decisions. Looking at finances only month by month, without considering seasonal cycles, can lead to wrong conclusions — like cutting the budget just when it’s time to invest in preparing for peak sales.

- Missed growth opportunities. Without seasonality analytics, a business focuses only on survival instead of using peak months for scaling — launching new products, increasing average check, or attracting investments.

Why It’s Important to Account for Seasonality in Financial Management

- For forecasting. Seasonality helps anticipate in advance when income will rise or fall — and prepare for it financially.

- For planning. Knowing when a downturn is expected allows you to create reserves in advance, adjust budgets, and avoid cash gaps.

- For expense optimization. Analyzing seasonal fluctuations shows which costs can be temporarily reduced and which should be strengthened during peak periods (for example, marketing, logistics, or procurement).

- For stability. A business that understands its financial cycles doesn’t react chaotically but manages cash flow consciously. This means less stress, more predictability, and a clear financial strategy for the entire year.

- For data-driven decision-making. When seasonal trends are recorded in numbers, management decisions stop being intuitive. The owner sees the full picture — which months bring the main profit, when to scale, and when to control spending.

How to Check How Much Your Business Depends on Seasonal Fluctuations

Seasonality can manifest in different ways, and business owners often notice it only after the fact — when there’s suddenly not enough money in the account and the number of clients drops.

That’s how financial stress begins — the kind that could have been predicted if you knew exactly when your business depends on seasonal fluctuations.

Don’t wait until the numbers tell you that something’s wrong.

Take a quick test and find out:

- whether your business has seasonality;

- how much it affects your money;

- and how you can influence it.

Does Your Business Depend on Seasonality?

Answer “yes” or “no” to the following questions to determine how much your business depends on seasonality.

At the end, count the number of “yes” answers — the result will show your level of seasonal dependency and help you understand how to plan your finances more effectively.

| Area | Self-Check Questions | Tip / Interpretation |

|---|---|---|

| 1. Client Work |

1. Do you notice sudden fluctuations in the number of clients without changing your ads? 2. Does demand shift depending on holidays, weather, or tourist seasons? 3. Are there months when the average check is consistently lower than usual? |

The answers help you analyze whether your demand has a seasonal nature. Check this in Finmap by comparing monthly revenue in the Cash Flow report. |

| 2. Team |

1. Does your team’s workload change throughout the year? 2. Do you sometimes need to hire additional staff? 3. Do you have to pay overtime during peak sales periods? |

Find out if your team’s workload follows seasonal cycles. Plan schedules and payroll budgets in advance. |

| 3. Purchases and Inventory |

1. Do order quantities change from time to time? 2. After active months, do you have unsold goods or write-offs? 3. Have you experienced product shortages during sales peaks? |

Identify whether your purchases have seasonal patterns. Track them in Finmap to see how much money gets frozen in stock. |

| 4. Cash Flow |

1. Are there months when income drops but expenses stay the same? 2. Have you experienced cash gaps in certain times of the year? 3. Are there periods when you need to use reserves to cover daily expenses? |

Control your cash more systematically. Finmap helps you forecast cash flow and avoid liquidity gaps. |

| 5. Marketing and Strategy |

1. Do you run promotions or discounts during slow periods? 2. Do you plan ad campaigns for specific seasons or holidays? 3. Have you noticed that ads perform better in certain months? |

If your marketing adapts to certain periods of the year, your business has seasonality. Analyze marketing expenses in Finmap to see which season brings the best ROI. |

How to Calculate the Result

0–4 “yes” — minimal seasonality. Your business has stable demand and steady sales throughout the year.

Recommendations:

- Keep a record of income and expenses to track long-term trends — markets and customer behavior change over time.

- Monitor your margins to understand the real profitability of each business direction.

- Automate your financial management in Finmap to avoid errors and save time on manual calculations.

5–9 “yes” — moderate seasonality. Your business partly reacts to seasonal changes or events, so it’s important to plan your cash flow in advance.

Recommendations:

- Create a financial forecast at least 3 months ahead.

- Build a reserve fund to cover low-sales periods.

- Analyze your revenue trends in the Cash Flow report in Finmap to clearly see when peak and “quiet” months occur.

10+ “yes” — high seasonality. Your business shows strong demand cycles. Without financial flow planning, regular cash gaps are likely.

Recommendations:

- Create a quarterly budget with income and expense forecasts.

- Allocate part of your profit to reserves for fixed costs (rent, salaries, taxes).

- Use the Plan/Fact report to spot deviations from your budget in time.

- Review your marketing strategy: maximize sales during peak months, and focus on efficiency during slow periods.

Financial Management Features for Seasonal and Non-Seasonal Businesses

Seasonality is not only about sales — it’s about how cash flow changes throughout the year.

In financial management, the difference between a seasonal and a stable business is significant — it determines the strategy for planning, budgeting, and building reserves.

How Financial Management Works in a Seasonal Business

- Irregular cash flow. Profits come in waves: peak months (holidays, tourist season) alternate with “quiet” ones. That’s why the owner needs to forecast cash to cover expenses during downturns.

- Planning by periods, not just by income. In Finmap, it’s important not only to record transactions, but also to forecast when income and expenses are expected. This allows you to allocate profit wisely — part for growth, part for reserves.

- Reserve fund as a must. In seasonal businesses, profitable periods should cover the off-season. The key metric is not monthly profit, but annual average profitability.

- Separate fixed and variable expenses. This helps you see which costs remain constant even during slow months (rent, utilities, admin salaries) and plan reserves accordingly.

- Analyze seasonal trends. The Cash Flow chart in Finmap helps visualize recurring sales peaks and adapt purchasing, inventory, and marketing plans.

This not only helps you stay stable, but also turns seasonality into an advantage — for example, by focusing marketing efforts when demand grows.

How Financial Management Works in a Non-Seasonal Business

- Stable cash flow. Income and expenses remain consistent throughout the year, allowing for simpler budgeting without the need for large reserves.

- Focus on efficiency. Such businesses prioritize the profitability of each direction, margin control, and cost optimization.

- Reserves are still necessary, but smaller. Even with stable sales, short-term disruptions can occur — for example, client payment delays. A reserve covering 1–2 months of expenses is enough to create a safe operational buffer.

- Strategic growth through analytics. In non-seasonal businesses, there’s more room for detailed analytics: comparing profitability across directions, identifying the most effective sales channels, and optimizing expenses.

- Continuous focus on marketing. Without natural seasonal demand spikes, marketing must run continuously. Owners should regularly analyze campaign performance to maintain stable sales levels and avoid gradual decline.

Comparison: Seasonal vs. Non-Seasonal Business

| Criterion | Seasonal Business | Non-Seasonal Business |

|---|---|---|

| Cash Flow | Uneven: alternating peak and quiet periods, requires a financial reserve. | Even throughout the year, allowing predictable income and expenses without major fluctuations. |

| Budgeting | Planned by periods and seasons. Part of the profit should be set aside for “quiet” months. | Planned by business areas and expense categories. Focus on accuracy and optimization. |

| Reserves | A key survival element: covers fixed costs during low seasons. | Minimal reserves — enough for emergencies. |

| Expense Management | Focus on separating fixed and variable costs to control cash gaps. | Focus on reducing inefficiencies and improving margins. |

| Financial Data Analysis | Important to track revenue cycles, sales peaks, and declines. | Focused on stability, profitability by segment, and long-term trends. |

| Marketing | Activity concentrated around peak periods to maximize profit. | Continuous marketing to maintain steady demand without natural spikes. |

| Main Accounting Goal | Anticipate fluctuations, maintain liquidity, and avoid cash gaps. | Improve efficiency and profitability, automate financial control. |

| Finmap Helps | Analyze seasonal trends, forecast cash flow, plan reserves. | Optimize regular processes, track profitability, and monitor marketing performance. |

Seasonality is not a threat — it’s a sign of a mature business.

Those who can anticipate their cycles turn peaks into profit and slow periods into opportunities for growth.

Which Tools Help Track Seasonality

To understand how your business changes throughout the year, you need not just numbers — but dynamics: seeing when sales grow, expenses increase, and cash gaps appear.

In Finmap, this can be done using several tools that reveal seasonal fluctuations from different perspectives.

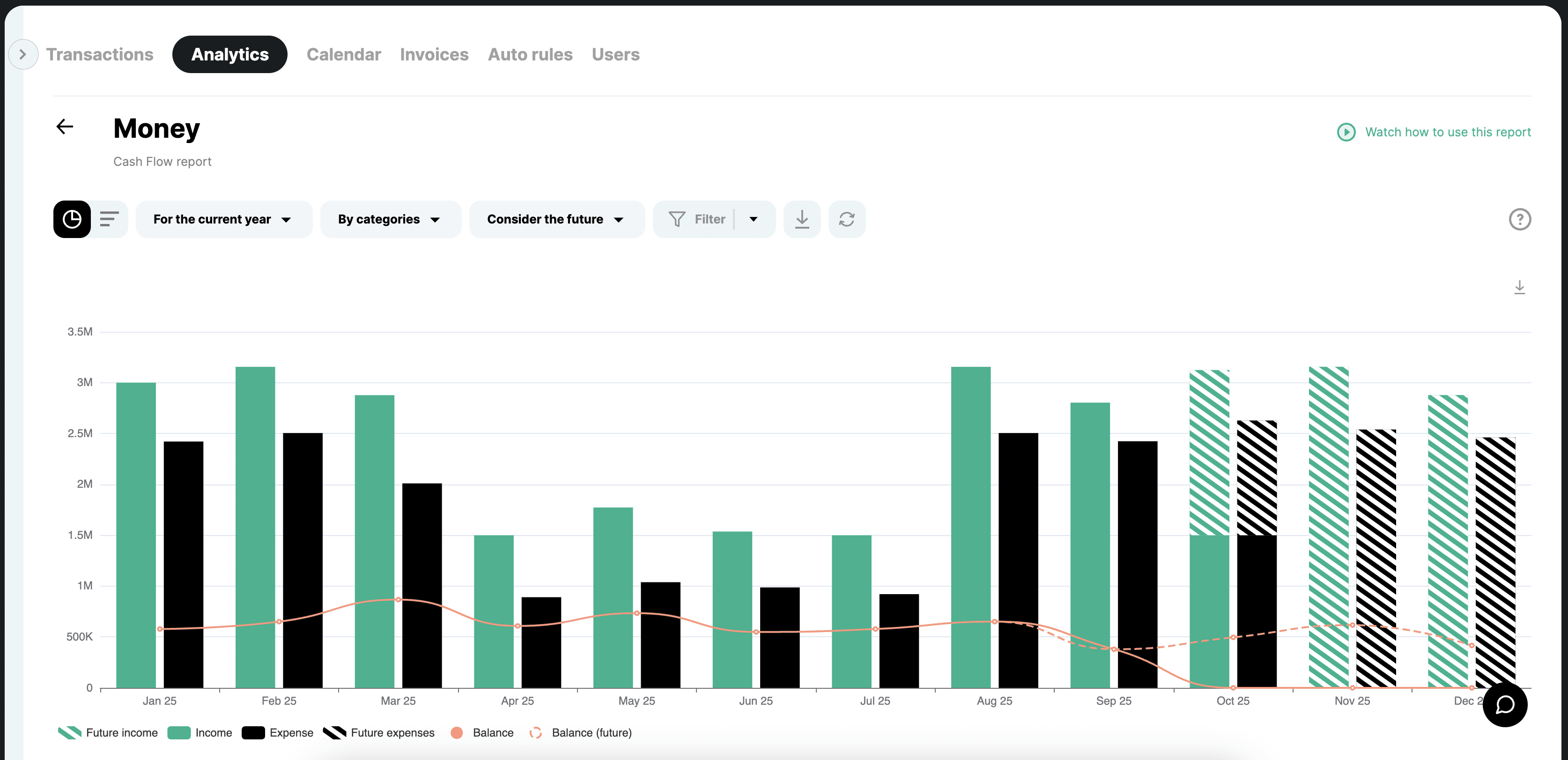

1. “Cash Flow” Report

The main tool for identifying seasonal patterns. The chart clearly shows how cash movements change month by month — income, expenses, and balances.

If certain months consistently show a rise or decline, that’s a clear indicator of seasonality.

Regular analysis helps you identify which periods are the most profitable and when it’s time to build up reserves.

2. “Inventory” Account

For businesses that manage stock, seasonality often appears in purchasing patterns and inventory levels.

By tracking inventory in monetary terms, you can see when cash is “frozen” in stock and when active sales occur.

This helps not only to control inventory turnover, but also to plan purchases for seasonal demand — without losing liquidity.

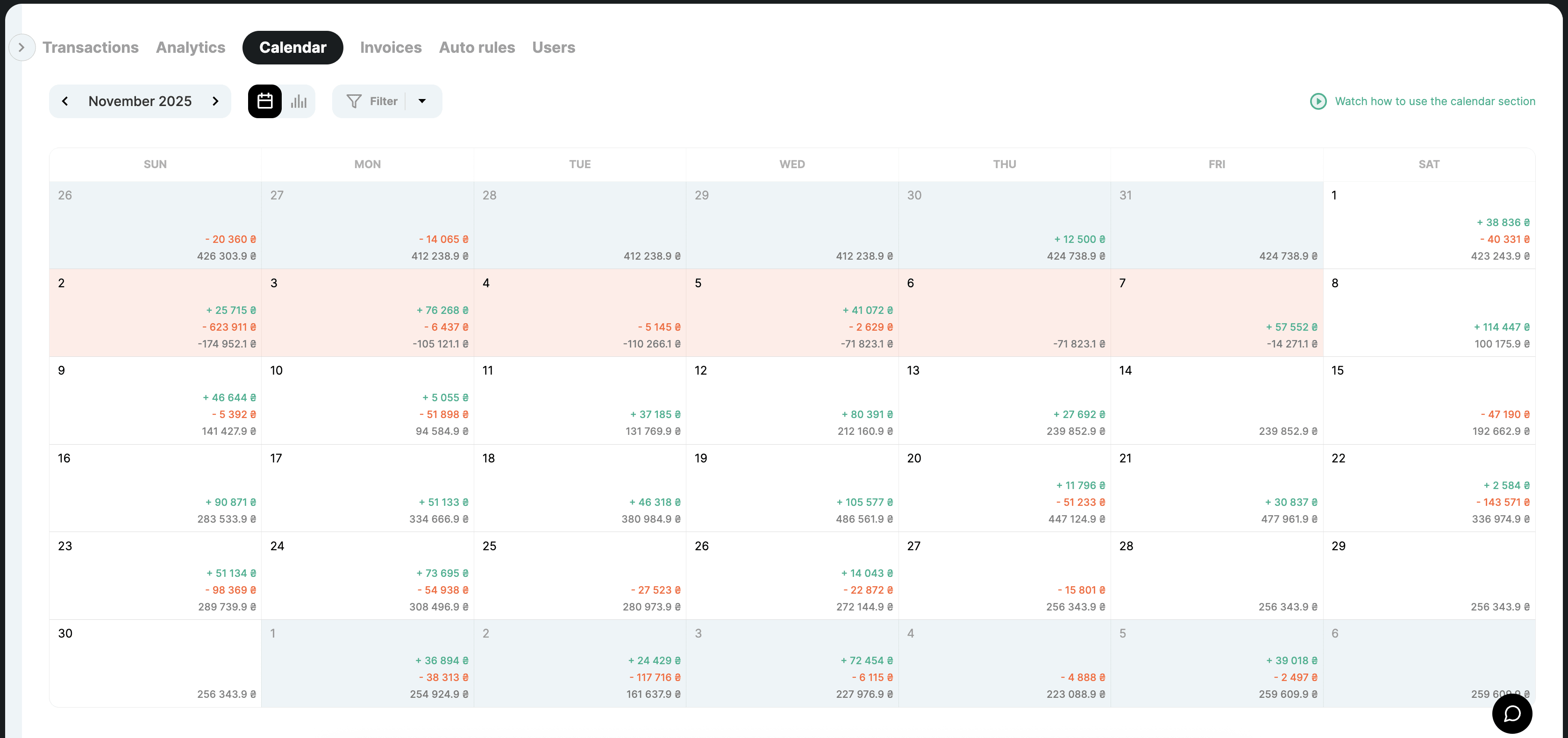

3. Planned Payments and Payment Calendar

Payment planning helps you prepare for the off-season in advance. The calendar shows when major expenses or inflows are expected and allows you to assess whether there will be enough funds to cover them.

This enables the business to distribute cash flow more evenly throughout the year and avoid liquidity gaps.

4. “Plan/Fact” Report

Comparing planned figures with actual results helps identify how seasonality affects budget performance.

If income in certain months significantly deviates from the forecast, this may indicate a seasonal factor.

Analyzing such deviations allows you to adjust your financial plan and better predict similar fluctuations in the future.

Tips for Businesses with Strong Seasonality

Seasonality isn’t just about revenue changes — it’s about shifts in the overall rhythm of the business.

When demand rises, you need to scale quickly; when it falls, you need to stay efficient.

To maintain balance between peaks and slow periods, it’s essential to have a systematic approach to finance, marketing, and operations.

Key Areas, Actions, and Management Decisions for Seasonal Businesses

| Area | What to Do | Example of a Management Decision |

|---|---|---|

| Marketing | Build your marketing strategy around demand cycles: scale reach during peak months, and focus on loyalty during off-season. | A furniture retailer reduces ad budgets in January–February but launches content campaigns to maintain brand visibility and attract long-term leads. |

| Assortment & Procurement | Analyze sales dynamics by category and adapt your assortment to seasonal trends. | A fashion brand places spring collection orders in autumn, using previous years’ sales data to avoid stock shortages. |

| Financial Planning | Build reserves during peak months to cover fixed expenses during slow periods. | A travel agency includes a mandatory reserve fund equal to two months of expenses after the summer season. |

| Team & Operational Efficiency | Prepare your team for peak periods and schedule training or workload balancing during off-season. | A manufacturing company conducts process audits and staff training (e.g., on inventory planning) during off-season before the next surge in orders. |

| Analytics & Forecasting | Analyze financial reports by month and year to identify demand patterns. | A retail chain compares 3-year sales dynamics in Finmap’s Cash Flow report to forecast next year’s revenue. |

You can’t eliminate seasonality — but you can calculate it, anticipate it, and turn it to your advantage.

When financial decisions are based on data rather than intuition, seasonality stops being a risk and becomes part of your strategy.

That’s exactly why Finmap was created — to help entrepreneurs see the full picture of their cash flow, plan ahead, and stay stable in any season.

Connect Finmap and turn seasonality from a source of stress into a source of growth!

Topic foundation: Cash Flow Gap: How to Identify It and How to Prevent It

Share valuable content — become a source of insights

Frequently Asked Questions

What is seasonality in business?

Seasonality is the regular, repeating fluctuation of sales, demand, or expenses across the year — common in retail, construction, services, manufacturing, and e-commerce.

Why is seasonality a financial risk?

Without planning for it, downturns cause cash gaps, over- or under-stocking, team overload or downtime, and poor decisions. In some industries, up to 70% of annual revenue comes from just a few peak months.

How do you plan finances around seasonality?

Measure how dependent your business is on seasonal swings, forecast demand, build reserves to cover fixed costs in low periods, and invest ahead of peak season instead of cutting budgets at the wrong time.

Any questions left?

We are ready to answer them.

Finmap support